Markets in a Minute - A Fighting Chance for Active Management

Key Takeaways

- Passive remains a strong portfolio foundation. Low costs and broad market exposure make passive investing hard to beat at the core. But index construction involves its own set of active decisions.

- Active has a better fighting chance than it used to. With costs coming down and more efficient structures in play, active management has a better chance to deliver alpha than before. The bar is still high, but it’s no longer as punishing as it once was.

- Active exposure should be sized intentionally, for both a risk and tax budget. Active management introduces tracking error and, in taxable accounts, can create realized gains. Investors should be deliberate about how much active risk they take and use tools like tax-loss harvesting and capital gains budgets to manage the tradeoffs.

The case for active management has been a difficult one. Markets are efficient at allocating capital, and over the long run stocks are driven by expectations of future earnings. With the rise of low-cost index products, investors have received cost effective exposure to markets. While index investing will never outperform, it enables investors to capture most of the market’s return—a powerful proposition.

Similarly, stock prices reflect the wisdom of the crowd, the aggregate expectations of all investors. In this light, active management had a huge obstacle to overcome. On expectation, you would expect most managers to fall short, and in fact that is exactly what we see over the long haul.

But active management has, historically, looked very expensive and highly dependent on the manager’s intuition about a handful of companies. But look closely and there is a new form of active management. With the rise of active ETFs, costs have come down and sophisticated products have become available to retail investors. Alpha (the value a manager adds) will always be elusive and difficult to capture. But when things change, we have a responsibility to test our assumptions.

So, what is the role of passive investing today, and what is the case for active management now?

The Historical Case for Passive Investing

Passive investing gained popularity for good reason. Index funds offered a simple solution: own the market, keep costs low, and accept market returns.

Studies such as the SPIVA Scorecards from S&P Dow Jones show the underperformance of active managers through time. This result holds across regions, market caps, and asset classes, though the degree varies.

Even more striking is what these studies show about persistence. When an active manager does outperform in one period, that success rarely repeats. Very few funds remain in the top half—or even the top quartile—of performers over consecutive multi year periods.

This creates a core challenge for active investing:

- It is hard to outperform.

- It is even harder to do so consistently.

- It is nearly impossible to know ahead of time who will succeed.

If skill were the main driver of outperformance, we would expect winning managers to keep winning. The data suggests that luck plays a meaningful role, especially over shorter periods.

I am sympathetic to the argument that there is skill in active management. The Medallion Fund does exist, even if we can’t invest with them. Bill Miller’s Legg Mason Value Trust did have 15 straight years of outperformance (although he, in the end, acknowledged that luck had some role in that run).

Stock picking is a human endeavor, and we see people with a wide range of skills across all human endeavors. Are we all equally good at basketball, at painting, or the piano? No, of course not! Those who work on those skills develop them over time. So, there is some intuition to give the same credit to active managers.

But the data tells us there is a huge amount of luck still involved, and we cannot differentiate luck vs. skill before a skilled manager reveals themselves.

Given this evidence, the case for low-cost passive investing was, and still is, strong.

The Case For Active: Costs Still Matter, but Active Has Improved

While the long-term evidence favors passive investing, costs are a major part of the story. Historically, many managers were able to beat their benchmark on a gross basis[SD2.1]. But active mutual funds charged high fees, and these fees created a steep hurdle that many managers could not overcome.

That landscape is changing.

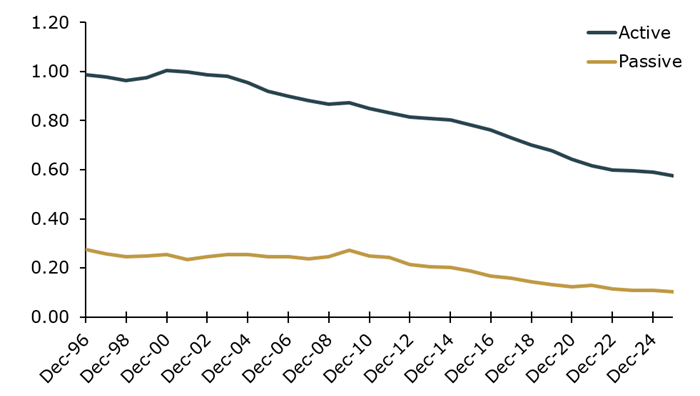

Exhibit 1 shows that investors paid lower fund expenses in 2025 than ever before, whether they owned active or passive funds. This should be celebrated, as it represents billions of dollars in savings for investors.

Exhibit 1: Active and Passive Management, Asset-Weighted Average Expense Ratios

Past performance is not a reliable indicator of current or future results. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from Morningstar. Data as of December 31, 2025 for US open-ended mutual funds and ETFs.

This is a welcome trend, but this does not make active investing “cheap”. Adding back the cost savings doesn’t mean the difference between underperformance and outperformance, between failure and success. But it does suggest that the headwind from fees is not as strong as it once was.

The Case for Active: Not Your Parent’s Active Portfolio

Another important change is how active management is practiced.

In the past, many active funds were expensive, concentrated, and highly dependent on bold forecasts—an uncompelling value proposition. Some took large risks without clearly explaining how those risks were managed.

Today, many newer active strategies look different. Many active strategies are competitively priced, broadly diversified, systematic in their portfolio construction, and have disciplined risk management.

These strategies do not rely on heroic stock picking alone. Instead, they focus on small, repeatable decisions that tilt portfolios toward certain characteristics, such as valuations, profitability, or balance sheet strength.

They also tend to pay closer attention to implementation details, such as trading costs, tax efficiency, and diversification. These improvements matter. Even small frictions can erode returns over time.

So we can’t just ignore all funds labeled active, as we may be missing portfolios that help us address the limitations of passive investing.

A Quick Detour to Discuss The Hidden Risks of Passive Investing

We would argue that all investing is active.

With passive investing, the perception is that you are only making one choice, and that is to invest in “the market”. That is misleading because each index defines and follows its own rules about which stocks are included and when. And those rules are subjective, and subject to change. The pending SpaceX IPO offers a clear example of this, as index providers are rushing to change their rules to allow for earlier inclusion and greater emphasis on this large and exciting IPO.

A simple truth is that an index is constructed by a series of active decisions. If an index is constructed with a series of active decisions, then choosing that index represents an active decision as well. Of course, passive investing has key characteristics, such as cost, that differentiate it meaningfully from active. But understanding that all investing is an active choice helps bridge the gap for those investors who are reluctant to incorporate active management.

Framing Portfolio Decisions: Return and Risk

At a high level, most portfolio decisions can be reduced to two questions:

- Am I improving expected returns?

- Am I mitigating risk?

Active strategies that only focus on the first question face a tough challenge. Beating the market is hard enough. Doing so without increasing risk is harder still.

Many active funds promise higher returns but deliver them only by taking on hidden risks. These risks may not show up in good markets, but they often appear during periods of stress.

A stronger value proposition comes from active strategies that address both questions at the same time. That may mean reducing downside risk, managing concentration, improving diversification, or managing taxes.

When viewed this way, active management is not just about beating the market. It is about how returns are earned.

Where Active Management May Make More Sense

It’s reasonable to believe that active management is more likely to add value in areas with less transparency, higher frictions or barriers, higher trading costs, or greater complexity

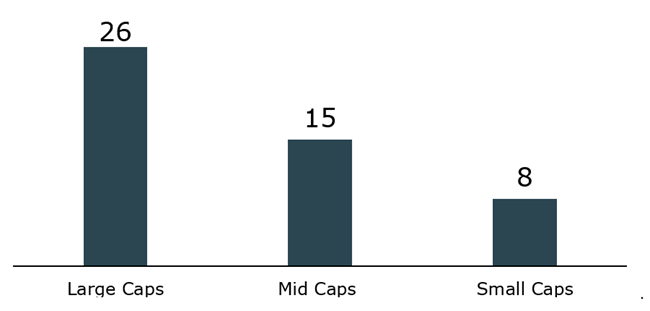

Several market segments such as small caps, international stocks, and fixed income fit this bill. For example, following the SEC’s 2003 enforcement on investment banks, coverage of small and mid-cap companies declined as the economics of that coverage changed. The result is that, today, far fewer Wall Street Analysts cover mid and small cap companies.

Exhibit 2: Wall Street Analyst Coverage – By Size

Source: FactSet and Kestra Investment Management. Data of the latest completed reporting period by company. Large Caps as represented by the S&P 500. Mid Caps as represented by the S&P 400. Small Caps as represented by the S&P 600.

“Number of Wall Street analysts” is an imperfect proxy for market efficiency. But different market segments have different characteristics, composition, and frictions to accessing them. In these environments, the flexibility of active management can add value over the rigidity of passive investing.

Budget For Risk, Budget for Taxes

Rather than asking whether to be active or passive, investors may benefit from a different question: How much active risk do I want to take?

Active management introduces uncertainty relative to the benchmark, so investors should treat it as part of a broader risk budget.

A balanced approach might look like this:

- Use passive funds for core, efficient exposures

- Add active strategies selectively, where the case is strongest

- Keep active allocations sized appropriately

- Focus on diversification across managers and styles

This framework avoids all or nothing thinking. It recognizes that active management is a tool, not a belief system./p> In addition to risk, the tax implication of active management requires thoughtful attention. Active managers can add value in ways that go beyond stock selection, through thoughtful position sizing and disciplined sell decisions for example. But that value comes with a cost. For investors in taxable accounts—particularly those using vehicles like SMAs that hold securities directly—these decisions can generate realized gains. A good problem, but still a real one.

The challenge is to manage that tradeoff deliberately. Investors can use tools such as asset location (e.g., active strategies in tax advantage accounts, passive in taxable), capital gains budgets and ongoing tax-loss harvesting, applied throughout the year rather than just in December, to help mitigate the impact. If the goal of an allocation to active management was the pursuit of manager alpha, then a plan to manage the resulting taxable gains need to be in place as well.

A More Practical Conclusion

Active management isn’t dead, but it isn’t something investors should reach for by default. Passive investing still offers a strong foundation, even if it’s far from risk-free.

Rather than picking a side, investors are better served by being clear about what each approach is meant to do and where it can fall short. Active strategies can add value, but it depends heavily on where and how they’re used. In the right context, they can complement a portfolio.

The real shift isn’t about declaring a winner between active and passive. It’s about being more intentional in portfolio construction—asking better questions about costs, risks, and implementation—and building portfolios that reflect those answers.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.